Dining: Mission Valley Bank’s Tamara Gurney eats a Crab Louie Salad at Runway at Hilton Woodland Hills/Los Angeles. (Photo by David Sprague)

Tamara Gurney is the chief executive and founding president of Mission Valley Bank, a Sun Valley-based community bank that opened in 2001. She sat down with the Business Journal at the Runway at Hilton Woodland Hills/Los Angeles for a power lunch to discuss her career.

Tell me about accounts receivable, which has become a huge product line for the bank. The accounts receivable product is a product to bridge cash flow gaps. A business owner has to make payroll, has to pay rent, has to do all these things while they’re selling their product, and they may not get paid on that product for 60 to 90 days…Accounts receivable will essentially purchase those invoices and advances them the money, and we collect on it when the buyer actually pays that invoice, and then everything settles up. That program has grown 200% in 18 months. Are there any upcoming regulation changes on your radar? There’s always regulation in our industry, and it just seems to continue to be more and more onerous, in particular, for small businesses like ours. Regulations start… with the behemoths, the 16 largest banks in the country. Unfortunately, once they’re implemented, they trickle down to smaller banks, and I keep trying to tell regulators that…when you look at Wells Fargo Bank, Bank of America and Mission Valley Bank, the only similarity between us and any of them is the word ‘bank.’ Our business models are completely different, and we need to be regulated differently. In the last year and a half, we’ve seen some big banks close and others merge. How has that affected Mission Valley Bank? We’ve had access to a number of prospective employees that are displaced… and clients as well, because they’re unsettled when their bank has failed or merged into another bank… Unfortunately, people don’t seem to rationalize the fact that Silicon Valley Bank was the 16th largest bank in the country… They categorized it as a smaller bank and seemed to migrate away from smaller, regional banks. So a lot of the deposits, a lot of the liquidity, went to the ‘too big to fail banks,’ and community banks like ours have struggled to maintain liquidity to keep the lending doors open. Looking forward, are you looking to grow organically or acquire other banks? In order to continue to grow deposits, we know we have to expand geographically. So we’re looking at where our clients come from outside of San Fernando Valley, which is our core market… We are evaluating the San Gabriel Valley and the South Bay area… If it made sense, we would look at an acquisition, but our growth right now has been organic.

Barry Pearlman of Pearlman, Brown & Wax in Encino. (Photo by David Sprague)

Barry Pearlman is the founder and managing partner of Encino-based employment law firm Pearlman, Brown & Wax. The firm, which has six additional offices, has been around for 40 years.

Pearlman owns a candy shop. Outside of his law practice, Pearlman co-owns AusSam Candy in Granada Hills. The shop is run by Austin Pearlman, Barry Pearlman’s son, and Samantha McDougall. The two are family friends who have known each other for decades. “Austin loves children and, after working in the film business for a while with kids with special needs (like himself) he wanted to open up a business. Samantha and Austin became partners and I assist as manager/member,” Pearlman says.

Pearlman started his firm with some parental aid. He decided to start his own firm after seeing some of the difficulties his father and brothers faced running a family business. Pearlman started his firm in 1984 with a $10,000 loan from his parents. The firm got its start in Tarzana and opened its headquarters in Encino in 1993.

He is active in the San Fernando Valley. Pearlman is a Valley native and he and his wife are very active in the community. Pearlman is a founding member of S.O.L.I.D., Supporters of Law Enforcement in Devonshire. The group helps the Devonshire division of the LAPD purchase equipment that there is not enough funding for.

He likes to mentor others. Pearlman says he likes to work with “the next generation of attorneys,” many of whom are Valley natives as well. His former partner’s son and his daughter are even members of the firm.

Many judges have come out of Pearlman, Brown & Wax. To date, 10 of the law firm’s attorneys have become workers’ compensation judges. Pearlman says some “see abuses in the system and believe they can assist by becoming judges.”

CHANDRA SUBRAMANIAM

Dean, David Nazarian College

of Business and Economics

California State University, Northridge. (Photo by David Sprague)

While there are plenty of stories about people and companies leaving California for states like Texas and its lower cost of living, in 2018 Chandra Subramaniam did the opposite, leaving the University of Texas at Arlington to become the dean of the David Nazarian College of Business and Economics at California State University, Northridge.

Since Subramaniam came to the university, his focus has been to create and expand programs to better the school.

Subramaniam has worked to expand the schools’ Career Education and Professional Development Center, which now sees more than 1,5000 students a year. The number of students using the center as a resource has increased over the last few years and the school has invested in AI-backed platforms to further help students.

“We are the only college within the campus that has its own career center and have been spending more resources on the career center,” he says, adding that he was looking to “raise the social skills of students.”

The school also has a Passport Program which looks to build networking skills and offer career building for undergraduate business students. The program was piloted from 2014 to 2015 with five students and now serves roughly 500 students.

Another push has been getting students certifications such as Google Ads and Microsoft Excel Expert.

“We are moving in a big way to make sure students are not only getting a degree when they graduate but while they are getting a degree earn a number of third-party certifications,” Subramaniam says.

Subramaniam has also been working to make sure the school’s offerings are in line with current market trends.

“For a business school to become known they need to make sure that they have the types of degrees that the market wants,” Subramaniam says.

In 2021, for example, the school created an undergraduate business analytics degree which now has 146 students. The school more recently launched a master’s program in business analytics as well.

Attracting diverse students

The Nazarian College has grown over the years and is now the ninth largest business school in the nation and one of the most diverse. In the 2020 to 2021 school year, for example, it was No. 3 in the nation when it came to awarding bachelor’s degrees to Latino students.

“We are a very diverse campus,” Subramaniam says, adding that the school is only 24% white.

Subramaniam says the student makeup at CSUN has varied from when he started. Five years ago there were “more transfer students than anything else” but he is now seeing more people come straight from high school as well. Still, the average student is 26, he says, adding that 70% of its students are first-generation college students.

“I believe that education has a purpose: to lift people up,” Subramaniam says.

“Every student that you help and support and get a job means something and they help the whole family and it raises the whole family,” he adds.

Subramaniam says it’s also important for students to find something they enjoy because “it’s something you are going to do for a long time.”

He adds that “a career is never a linear line” and that it’s important to be willing to adjust.

Subramaniam got his degree in physics and worked at the National Semiconductor in Malaysia. He worked his way up and realized how important management was, so he went back to school to get an MBA. He later earned a doctorate and went into education.

Subramaniam is now looking ahead toward the future of CSUN.

“The next few years for us is going to be a fascinating period. We have moved the needle a lot at the college over the last five years…now the question is, where do we move the college over the next five years?” Subramaniam asks. “Part of that and one of the things we are trying to achieve is add on to the building we have to add on to the ecosystem.”

“A college or university like CSUN, our primary role is to ensure that all students can get the education they deserve and want, and the question becomes how do we help them become successful,” he adds.

DANONE SIMPSON

Founder, Chief Executive

Montage Insurance Solutions. (Photo by David Sprague)

A chance misunderstanding guided Danone Simpson to the insurance industry.

Having spent 17 years as an actress, model and events planner, Simpson says she reached a crossroads where she wanted to work in a “have to have” business – an operation that provides an essential service. She settled on what she thought was an advertising agency she’d seen featured in a magazine. When she walked into the company, she found it was actually an insurance brokerage.

During the interview, she recalls being bothered by the files haphazardly stacked on the floor. So she offered to clean it up for the manager.

“I literally sorted his files for him and got the job, even though I didn’t have any experience,” she says.

Simpson hit the ground running with that job, working the phones and learning what the company’s clients truly needed. The firm handled both benefits as well as property and casualty, a relative rarity in the industry.

“I could shift to whatever the client needed,” she says.

Simpson learned enough to eventually form Montage Insurance Solutions in 2006, a firm that consistently ranks among the top in the San Fernando Valley area in terms of local premiums.

Her company’s success comes from a formula of offering highly customized plans, even among clients that seem at first glance to have a lot of overlap.

“I don’t care if two of our charter schools do the same thing,” she says, as an example. “Basically, they’re very different the way they manage their employees or where they’re located.”

Among other areas, Montage also handles insurance brokerage for private schools, credit unions, nonprofits and manufacturing companies.

“It is really about making sure that they’re properly insured, and that they have the insurance coverages that they need,” she says. “The market is hardening right now, finally. They’ve been talking about it hardening for years, but it is finally happening. There are so many disasters all over the world, but here in the U.S., especially, so our carriers have been impacted greatly.”

California is underinsured

Such has been the case in California, a state known in the industry, Simpson says, to be largely underinsured. The number of natural disasters like wildfires and flooding that have hampered the state in recent years have made property insurers wary, to the point of freezing policy renewals or outright leaving the market. On the medical side, patients continue to make up for lost time after hospitals and medical centers needed to diverge non-urgent or elective procedures during the height of the Covid-19 pandemic.

Simpson started her company after varying experiences with other brokerages that left her discouraged. One company, she says, would tack on extra fees for clients and selectively disclose available plans. She also took note at another agency, she recalls, when management suddenly laid off three women about when they turned 50.

“I think the most important thing to me as a woman-owned company is valuing the employees,” Simpson says. “They need to feel safe and cared for. That is really critical.”

Transparency is another key for Simpson, one she thinks makes her company successful. Montage agents present every available offer to potential clients and also disclose whatever commissions the company will receive from the provider. The company also requests denials in a letter or email so that it can provide them to prospective clients.

“A lot of brokers just go in and show them what they think the client might like,” she says. “I let the client make the decision. I show them everything.”

It seems to be a winning formula. Montage employs 27. Many of its employees have clocked in well over a decade with Montage, and Simpson says there is a similar loyalty from clients.

A sister company, Simpolicy, works with employers with 50 and fewer employees. Simpson is also in the process of having an auditing software, to be titled Bene, developed to help companies audit various insurance bills.

“I’ve been doing auditing since I started the business, I thought it was really important to help our clients audit their bills,” she says. “So now we’re just creating a solution to help do it faster.”

MICHAEL OLENICK

President, Chief Executive

Child Care Resource Center (Photo by Rich Schmitt)

When Michael Olenick became the president and chief executive of Chatsworth-based nonprofit Child Care Resource Center, he managed a staff of 300 and $89 million. In 21 years, the staff quadrupled and the budget grew to $700 million.

“You have to kind of run it like a business,” he says.

Although he grew up in the child care space – his mother was a childhood development professor in Chicago and previously ran a slew of preschools– Olenick spent his early to mid-20s chasing the rock and roll fever that swept over U.S. during the late ’60s. He played electric violin in a band that opened for REO Speedwagon and collaborated with Sam Lay from the Paul Butterfield Blues Band.

When Olenick left that world in his late 20s, he studied social programs and how to make them successful. He got a part-time job evaluating why foster parents weren’t going to foster parent training classes at the community college, and determined someone needed to act as a liaison between the Department of Children and Family Services and these community colleges.

From there it was a snowball effect. He ended up taking on that very role and began running half a dozen family and children programs for Los Angeles County and the community college network.

When the Community College Foundation switched leadership, Olenick was suddenly running programs in 60 to 70 different colleges statewide.

A well-oiled machine

When Olenick took over the CCRC, the organization was in shambles. It was being sued by the state and dealing with internal fraud issues.

“We didn’t have certain processes in place,” Olenick says. “The state did a forensic audit on us and said, ‘you’re charging too much for this or for that and you owe us $2 million.’”

Olenick removed several high-level employees from the organization and diversified revenue streams in order to streamline the nonprofit.

Running a nonprofit like a business took some getting used to. Olenick had to reject program ideas that were projected to always be in a deficit.

“And they all looked at me and said, ‘but we’re here to do good,’” he recalls. “You can’t do good if you run yourself into the ground.”

There was also a culture problem. Olenick said staff feedback at CCRC mentioned executives never smiled.

“So I always made sure that when I walked in that door, no matter how I feel coming in, it’s showtime,” he says. “I say hello to everybody that I see.”

As CCRC grew, it switched over to updated administrative programs that could handle more projects. It had to create online portals for parents to find child care that fit their specific needs. It also meant keeping an eye out for trends that could disrupt the operation.

As more families moved to San Bernardino County, the CCRC began expanding its programs geographically. In the years following Covid-19, agencies noticed more families migrating out of L.A. County. (Indeed, the Los Angeles Unified School District’s Board of Education predicts enrollment will drop 30% in the next decade.)

“(Agencies) located in Los Angeles are really struggling with where the kids are going to be in the next few years. How can they sustain what they’re doing?” Olenick says. “Whereas we’re okay. We made the moves before anybody even thought about it.”

Olenick is looking ahead in other ways, too.

“I’m kind of getting up there in age,” Olenick says. “So I’m trying to make sure that, over the next five years, if I leave, the organization will not fall apart.”

The CCRC serves around 50,000 kids and families a month. It also has a team of five stationed in Sacramento to work on policies and legislation.

And it is still growing. The nonprofit is looking into providing Head Start services for children for whom CCRC pays for child care services. It’s also making strides with with medical providers in L.A. County to provide health care services for families in its network. CCRC itself in the process of becoming a Medi-Cal provider.

“You build this really big engine, you don’t want to see it die,” Olenick says. “You want it to outlive you, right?”

MICHELLE

GASKILL-HAMES

President

Kaiser Permanente

Southern California and Hawaii. (Photo by David Sprague)

After a literal trial-by-fire start last year to her tenure as president of Kaiser Permanente Southern California and Hawaii, Michelle Gaskill-Hames is now focusing on growing the giant hospital system’s facilities and services throughout her territory, including the greater San Fernando Valley region.

Kaiser Permanente, with 10,500 workers stationed in the greater San Fernando Valley area, was second only to the Walt Disney Co. on the Business Journal’s list of largest private sector employers in the Valley area, published last August. It operates large medical centers in Woodland Hills and Panorama City in addition to a number of smaller offices and facilities in the Conejo, Santa Clarita and Antelope valleys.

Recently, Kaiser Permanente has opened a new surgery center and medical office space in Lancaster, new space in Woodland Hills for behavioral health treatment and expanded emergency service and imaging capabilities at its Panorama City medical center. And on the horizon is a new medical laboratory in Santa Clarita.

These are all part of the Oakland-based health system’s $290 million investment over the last five years in the Greater San Fernando Valley region.

“We are committed to continuing to serve our members with high quality services across the Valley,” Gaskill-Hames says. “We have our energy solely focused on growth and improving the member experience.”

Hawaii wildfires

Gaskill-Hames was named interim president for Kaiser Permanente’s Southern California and Hawaii region in April of last year and full-time president in September. She replaced Julie Miller-Phipps, who retired after seven years in the post. Gaskill-Hames oversees nearly 78,000 employees who collaborate with more than 8,000 Kaiser Permanente Medical Group physicians to deliver care to roughly 4.8 million members through 15 hospitals and 236 medical offices in Southern California, as well as another 268,000 members in Hawaii.

Prior to this post, Gaskill-Hames held several executive positions with Kaiser Permanente, primarily in Northern California. Before joining Kaiser in 2016, she served in several executive posts at other hospitals, most notably at Northwestern Memorial HealthCare in the Chicago area.

Just three months after being named interim president for Kaiser Permanente Southern California and Hawaii, devastating wildfires broke out around the town of Lahaina on the Hawaiian island of Maui. With much of the island paralyzed for months, Gaskill-Hames had to lead the effort to ensure all of Kaiser Permanente’s facilities remained operational, which meant bringing in more resources from outside, including a mobile care vehicle from California.

New Lancaster Surgery Center

That effort understandably diverted some attention from all of the growth initiatives that Gaskill-Hames had to oversee in Southern California, including the Greater San Fernando Valley region.

One of the biggest efforts has been the leasing and opening of 12,532 square feet of surgery center space in a building in Lancaster. Kaiser Permanente assumed the lease in February and spent four months getting the center ready.

Up until now, Kaiser Permanente has had only medical office space in the Antelope Valley – though that space is substantial at roughly 290,000 square feet across four sites. If Kaiser members in the area needed surgery, they either had to go to other Kaiser medical centers in the county or to non-Kaiser hospitals in the Antelope Valley.

“This allows us for the first time to have our own surgical facility in the Antelope Valley,” Gaskill-Hames says.

The surgery center, which opened in June, is only for scheduled surgical procedures; emergency surgeries must still be handled by nearby non-Kaiser hospitals.

Other facility enhancements

Over the last 18 months, Kaiser has added several services to its Panorama City and Woodland Hills hospitals. Among these are an expansion of the emergency department at Panorama City with new triage rooms and imaging equipment as well as a new neurology center at Woodland Hills that includes an outpatient clinic.

Also in Woodland Hills, Kaiser Permanente last year opened a 15,000-square-foot behavioral health facility at a separate location from the hospital. Gaskill-Hames says that opening this center means members no longer have to travel to Kaiser Permanente’s regional flagship hospital in East Hollywood.

Finally, Gaskill-Hames says Kaiser Permanente is working to open a new regional medical laboratory in Santa Clarita late next year. Kaiser has leased a 223,000-square-foot building for the lab. A Kaiser spokesman says details on the lab were still being worked out, including whether the lab would be accessible for members or whether it would be more of a back-office operation for lab technicians.

“It will serve as an integral part of our regional lab network, enhancing our capabilities and service offerings for our members in the Santa Clarita Valley,” spokesman Terry Kanakri says.

Beyond these measures, Gaskill-Hames says Kaiser Permanente is evaluating whether to open more health clinics in outlying neighborhoods in coming years.

“Our members have indicated they want convenience and ease in accessing the health system’s facilities,” she says. “We’re constantly looking at ways to make what’s big feel small.”

Miri Rossitto, CEO of Cowe Communications. (Photo by David Sprague)

Miri Rossitto is the founder and chief executive of Cowe Communications, a Calabasas-based business and brand-development firm. During the course of her career, she has made a few mistakes. Here, she talks about being resilient and not doing things alone.

—

The path of my career has been paved with the shattered remnants of my optimistic ego. It was never my intention to own a communications firm because my childhood dream was to go into the medical field (first mistake). As it turns out, my inability to get beyond fifth-grade math made “Dr. Miri Rossitto” an impossibility, so I turned to the next obvious choice: journalism (second mistake). I tried that path too for a bit, but I was incredibly unhappy just learning in a classroom. I wanted – no, needed – to get my hands dirty. And so, I became an entrepreneur.

To me, entrepreneur is just a fancy way of saying “someone who willingly signs up for a rollercoaster ride of punishment and pain.” Why is it so excruciating? Mistakes! So. Many. Mistakes. From the moment I wake up until the moment I pretend to sleep for three hours, I do nothing but orchestrate new ways for other people to say to me, “Really, Miri?!”

Interestingly, amidst the chaos, I discovered my superpower: resilience. The countless embarrassments I endured wove a coat of confidence around me, but had I not experienced my biggest mistake early on, I certainly wouldn’t be here today telling you this cautionary tale.

Miri Rossitto, CEO of Cowe Communications. (Photo by David Sprague)

Trying to be a lone wolf

When people think of an “entrepreneur,” they typically think of a lone hero who bravely scales the impenetrable walls of business all by themselves. This was how my ego and I viewed entrepreneurship when we started this company: with a vision that it was going to only be my way and that other people were a liability and distraction. What an epic and costly mistake that turned out to be.

I buried the headline, so let me just say this now: There is no success without a team. Not one entrepreneur, not one company, not one anything is successful without a team. Sure, there are dysfunctional teams, but the fact remains that truly nothing impactful or important happened because one person did it all by themselves.

Nine years ago, I was convinced that I knew best. I was going to save so many businesses all by myself because of me, me and me. My prior 20 years of repeatedly making mistakes in business clearly positioned me to help others avoid the same humiliation. How wrong I was. It took me two painful years and $150,000 to figure out that while I could develop game-changing ideas, none of them could be executed without a team. My biggest mistake wasn’t prioritizing and investing in a talented team of my own for far too long and not realizing that outstanding teams were undoubtedly the solution to almost every client problem that I encountered.

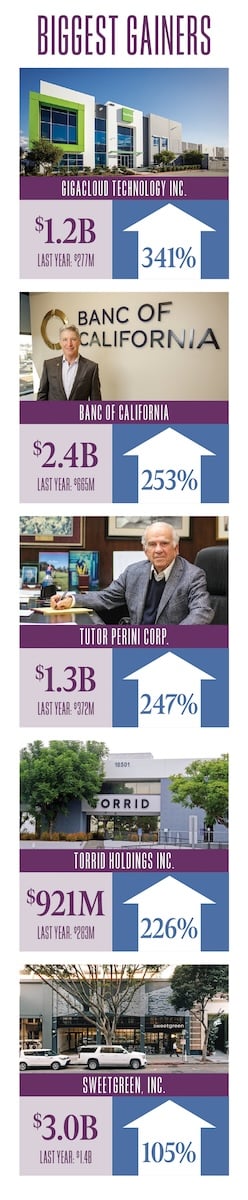

L.A.’s 60 largest public companies fared reasonably well on Wall Street over the past year, but not as well on Main Street.

These 60 companies collectively managed to hold their own for market performance, posting a 20% jump in market capitalization over the past year to $737 billion, according to an analysis of market cap data for the Business Journal’s annual list. That was slightly below the 26% gain for the Standard & Poor’s 500 index and the 25% increase in the broad Russell 3000 index; these two are the most similar to the mix of companies on the Business Journal list.

Revenue growth was more modest. Collectively, the 60 companies posted a 7.3% gain in revenue last year to nearly $307 billion.

But net income, which measures profitability, fell last year by $5.45 billion, or 25%, to a collective $16.5 billion. Just over half (31) of the 60 companies saw net income drop in 2023 compared with 2022, including several that reported bigger losses than in the previous year.

No company better exemplified this split performance than Brentwood-based Banc of California Inc. This regional bank was the second biggest percentage gainer in market cap on the list, jumping 253% to $2.35 billion. But it posted a 79% drop in revenue last year to $278 million, while swinging to a loss last year of nearly $1.9 billion as the bank struggled with underperforming loans.

Granted, the time frames were slightly different (June 30 of last year to July 15 of this year for the market cap and calendar year 2022 to 2023 for the financial metrics), but there was still a six-month overlap.

Last November, the bank merged with PacWest Bancorp and finances have since stabilized; the bank holding company last week reported second quarter net income of $20.4 million, while net income for the first half of this year added up to $41 million.

Returning to the Business Journal’s market cap list, 43 of the 60 companies on the list posted gains in market cap between June 30 of last year and July 15 of this year, the time period analyzed on this year’s Business Journal list.

The biggest gainers in dollar terms were biotech giant Amgen Inc. (up $58 billion to $177 billion), Walt Disney Co. (up $24 billion to $187 billion) and private equity firm Ares Management Corp. (up $9 billion to $26 billion). Amgen’s gain was in part due to federal regulators finally approving its acquisition of Irish pharmaceutical company Horizon Therapeutics.

On a percentage basis, the biggest gainers were GigaCloud TechnologyInc. (up 341% to $1.22 billion), Banc of California (up 253%) and Tutor Perini Corp. (up 247%).

The biggest market cap losers in dollar terms were biotech firm Acelyrin Inc. (down $1.42 billion), toymaker Mattel Inc. (down $1.18 billion) and Kennedy-Wilson Holdings Inc. (down $993 million).

Acelyrin was also the biggest percentage loser, shedding 70% of its market cap. In September, the Agoura Hills-based biotech firm announced that its lead drug candidate to treat skin diseases failed to show significant positive results in a late-stage clinical trial.

Other major percentage losers were Kennedy-Wilson and Fulgent Genetics Inc. (down 44% and 43% respectively).

On the revenue front, 43 of the 60 companies on the Business Journal list recorded gains in revenue, led by a jump of $6.18 billion at Walt Disney Co. and $6.07 billion at Live Nation Entertainment Inc.

Banc of California’s $1.06 billion drop in revenue was the largest, followed by Edison International (down $882 million) and Marcus &Millichap Inc. (down $681 million).

On a percentage basis, Banc of California had the biggest revenue drop, followed by Fulgent Genetics and Marcus & Millichap, both falling around 53%.

Last year, 17 of the 60 companies lost money. Again, after Banc of California, Snap Inc. posted the biggest loss of $1.32 billion, followed by Lions Gate Entertainment Corp. with a loss of $1.1 billion).

Making an Exit

Two companies, previous staples of the list, did not qualify this year.

Last year Microsoft Corp. purchasedActivision Blizzard Inc.for $69 billion. Activision, which is based in Santa Monica, is one of the largest video game studios in the world. Its titles include “Call of Duty” and “World of Warcraft” and it owns a number of smaller studios in the area. Last year, it ranked No. 3 with a market cap of $65 billion.

And legal and management tech companyLegalZoom.com Inc.in April became the latest corporation to leave Los Angeles County, taking with it its then market cap of $1.26 billion. After calling Glendale home since 2010, the company relocated its headquarters to Mountain View while still maintaining some local operations. It was founded in 2001 by, among others, attorney Robert Shapiro – a key member of O.J. Simpson’s “Dream Team” of defense counselors. LegalZoom was the No. 35 company in last year’s list, with a market cap of $2.4 billion.

President/CEO Charlie Tourtellotte and Managing Director Chris Tourtellotte of LaTerra Development in Century City. (Photo by David Sprague.)

Despite overall market shakiness, one company is confident in the increasing demands for both housing and self-storage units. Century City-based LaTerra Development LLC, which has an estimated $3 billion portfolio value, specializes in both and has lately been heavily invested in Burbank.

The company is currently developing Intro, a 573-unit apartment complex that caters to Burbank’s media production tenant base. Made up of two buildings, Intro will host a variety of creative amenities, including writers’ lounges, getting ready rooms, movie theaters, green screens, podcast rooms and more. It is set to open by the end of the year.

Since its inception in 2009, LaTerra has also targeted select Sun Belt markets and during the pandemic launched its own self-storage platform.

Its founder and chief executive Charles Tourtellotte and his son, managing director Chris Tourtellotte, sat down with the Business Journal to discuss developing these two asset types, the lure of Burbank and what has caused the company to expand outward, nearly pausing operations in Los Angeles proper.

LaTerra specializes in both residential and self-storage facilities. What do you see in these two very distinct asset types?

Chris Tourtellotte: We view both of them as being essential. Everybody needs a place to live. The residential vertical has been the company’s DNA and the company’s roots for a long time. We like providing housing for people and creating spaces and creating homes for people to live and create memories. That’s rewarding and it’s tangible. And there’s always going to be a need for that in California, in Los Angeles and the markets we operate in. There’s a big shortage of housing. California is way behind on its housing production. There are a lot of supply constraints. It takes a really long time to get projects approved so California is really behind on its housing production.

And it became clear to us as time went on that there’s a really big need for more self-storage in Los Angeles. If you look at the metrics, Los Angeles is one of the lowest in the country. It has one of the lowest amounts of supply and it’s very dense. There are a lot of people. And the great thing about self-storage is it doesn’t compete with residential. The zonings don’t conflict. In fact, it’s very synergistic. The more housing we develop, the more there’s a need for storage.

You currently have a big apartment complex being bult in Burbank. Tell me about it.

Charles Tourtellotte:It’s the biggest one that we have under construction. It’s 573 units, 69 of them are moderate income. And we have another one that’s fully entitled in Burbank that’s 862 units. We haven’t started construction (on that one) but we’re close to starting and we’re just finishing the bidding on it now. That would make us the biggest residential developer in Burbank.

What kinds of amenities are in highest demand?

Chris Tourtellotte: Private open space is really important following Covid. If it’s an apartment project, that could be patios and balconies. Those are important. I think rooftop decks are important. People love a cool rooftop deck that’s well done with good views. If you can put a pool up there, people like pools, that’s a good amenity. In-unit washer and dryer are important. Fitness centers, people like fitness centers.

1 of 2

Rendering: Intro, LaTerra’s 573-unit development in Burbank.

Rendering: Intro, LaTerra’s 573-unit development in Burbank.

What’s most attractive about Burbank?

Chris Tourtellotte: Burbank is one of the best apartment markets in the country. It’s got 150,000 jobs but only 40,000 households. It’s like three and a half jobs per house, which is the highest jobs to housing ratio in any city in the country that I’ve come across.

Charles Tourtellotte: It’s much needed housing. Burbank is one of the many cities in California trying to comply with the RHNA requirements, which is the regional housing needs assessment standard for the state. And they’re under pressure, like all cities, to produce housing by certain timeframes. Each city has their own numbers that they have to hit by a certain timeframe. Burbank is one of them. We’re helping them get those requirement numbers.

What other submarkets are you interested in and why?

Charles Tourtellotte: Well, let me say this about Burbank versus let’s say city of Los Angeles. Why we like Burbank is it’s not in Los Angeles. We’ve had a long and good love affair with the city of Los Angeles. We’ve done a lot of projects in the city, but most recently, it’s become very difficult to do business in the city. It’s hard to process things here. It takes a long time. They’re just not set up to process our development projects.

LaTerra has expanded outside of California, targeting the Western Sun Belt states. Why these areas?

Charles Tourtellotte: We like to go where the jobs are. Now, Los Angeles and California have some jobs. There’s no doubt about that. There is a good employment base. There are universities here too that create this sort of perpetual, ongoing growth here. And we have a lifestyle which is driven mostly by weather. We’re not stopping here, but we’re looking to scale and grow the company. One way to do that is go ‘what are the other places that have jobs and have lifestyle? Where do people want to go?’ And it’s some of the Sun Belt cities. Not all of them, but some of them.

Leaders: LaTerra’s Charles and Chris Tourtellotte. (Photo by David Sprague)

Has Measure ULA spurred further expansion?

Charles Tourtellotte:Without a doubt. It’s caused us to go to other places. It’s housing that’s difficult. Two thirds of America’s jobs are created by entrepreneurs, guys like me who start businesses on their own. Those are the people who are moving out of Los Angeles. And I’m just going to caution, even the state of California is a very high tax state to do business in. For guys like me who live here, we pay a lot of tax. If you overtax, my word of caution to both the state, the city, the county, everybody here in California, be careful. Because you’re going to take away all the incentives for people to do business here. And that is going to be a big mistake.

What are your thoughts on adaptive reuse? Are any of your projects examples of adaptive reuse?

Charles Tourtellotte:Not in the residential area. We’re doing two, though, for storage. And I would say, because I know it’s a topic, converting say office to residential as adaptive reuse has not yet proven for us to be something that makes sense. It just is expensive and gets to be an unknown in terms of design and cost. If you take an office building and start looking at it and the floorplate, how the heck do you turn it into apartments? There’s been a few, but only very few, that I think you can point to that have been successful. It’s very difficult. It’s easier to just knock the building down and go ground-up new.

Chris Tourtellotte: Asset values are down. Apartment building values and other asset values are down let’s say 20% to 30% from early 2022 peak values. We have a strategy now of buying – not just developing – but buying existing apartment buildings that are completed and leased as a third line of business for us. Buying existing apartment buildings for less than replacement costs. We’re raising capital for that strategy. We’re actually hiring a head of capital markets in investor relations and we’re going to bring in more high net worth capital and family office capital for that.

Self-storage is an interesting asset type. It was doing well during the pandemic. How has it faired since?

Charles Tourtellotte: It’s beginning to improve. And I think it is tied to the overall residential market. As residential expands and contracts, so in part does storage. Storage does well in most markets. It’s a bit recession proof, which is one of the reasons we like it. We’re bullish on it. But even more bullish coming up for the near term because we think that as economic cycles shift, which we think it is about to, then capital will snap back in and come back in all regards, including storage. So that means valuations are going to change again. We think this is a good time for us to be building and buying. We think it’s a good time to put a shovel in the ground.

What’s it like to work together, father and son?

Chris Tourtellotte: It’s very rewarding. We have a nice time together. I think it’s very special.

Charles Tourtellotte: For me, it gives me a reason to get up every day and work hard and build the business. Which sort of was the shift for me when Chris came to work here because there was a time where I thought ‘maybe I’ll just sell the business.’ And then when Chris came, I said, ‘no, we’re going to build the business’ and there will be a generational shift. We’ll build the business into a generational business. Chris has added a ton of value. He’s really added a whole new dimension to our company. I’m really loving it.

What’s next for the company?

Charles Tourtellotte:I think this third vertical line of business, which is investing in existing buildings. I think that is our most exciting (new venture). That and continuing to grow the self-storage development platform.

Boss: Teledyne Executive Chair Robert Mehrabian. (Photo c/o Teledyne Technologies)

Teledyne Technologies Inc. reported its second quarter financials last week and got a boost to its stock price as it beat Wall Street estimates on both earnings and revenue.

The shares of the Thousand Oaks aerospace, marine and digital imaging products manufacturer increased by nearly 4% on July 24 to $417 on the day it released its financials before the market opened. The stock had closed at $402.27 on the previous day.

The company reported on July 24 that it had adjusted net income of $219 million ($4.58 a share) for the quarter ending June 30, compared with adjusted net income of $224 million ($4.67) in the same period of the previous year. Revenue decreased by almost 4% from the second quarter of the prior year to $1.37 billion.

Analysts on average expected earnings of $4.49 on revenue of $1.36 billion, according to LSEG, a provider of financial markets data.

The stock closed at $415.70 on July 25 or about a fraction of a percent increase year over year.

Robert Mehrabian, executive chair of Teledyne, said that its earnings exceeded expectations, orders were greater than sales for the third consecutive quarter driven by aerospace and defense work and that the company ended the second quarter with a record backlog.

“Therefore, we are reasonably confident that quarterly sales will again increase sequentially, and we will return to year-over-year growth in the second half of 2024,” Mehrabian said in a statement.

During a conference call with analysts to discuss second quarter earnings, Mehrabian said the results were a testament to the strength of its balanced business portfolio.

“We also continued our proven strategy of increasing margins in those businesses that are growing while reasonably protecting margins in those businesses with more challenging markets,” Mehrabian said.

Guy Hardwick, an analyst with Freedom Capital Markets in New York, asked about the free cash flow issue and how the company will look back on this year in terms of how it spent that money, either on paying down debt, acquisitions or buying back stock.

Mehrabian said Teledyne’s debt payments are fixed and that there is only one payment of $150 million due in October.

“Other than that, our payments start in 2026. And if you roll everything that we owe over the years, our interest payments are about 2.35%,” Mehrabian said.

For the rest of the year, the company will likely continue buying back stock, he said.

“We expect to continue to do that, but we’re also looking at acquisitions at the same time,” he said. “So, we’re balancing the two as we go forward right now… we think that we’re in a really good situation.”

The company has renewed its line of credit for another five years but hasn’t touched it yet, and has about $1.2 billion at its disposal, he continued.

“So, with no debt payments, big ones coming due, our interest rates being 2.35% over the many years, we feel good that we can do whatever we want,” Mehrabian said. “Right now, (we’re) focused on buying back stock and looking at acquisitions as well.”